DraftKings Q1 2026 Growth: What the Numbers Really Say

If you follow online gambling stocks, quarterly updates can feel noisy fast. Revenue jumps, customer metrics rise, and executives talk up momentum. But DraftKings Q1 2026 growth matters because it offers a clearer read on where the US betting market is heading right now. The company reported stronger top-line performance, pointing to more customer activity and a business that still has room to expand even in a tighter, more competitive market.

That matters whether you are an investor, affiliate, rival operator, or just tracking the health of sports betting and iGaming. A good quarter does not answer every question. It does, however, show where DraftKings is gaining ground, where pressure still exists, and what the company needs to prove next.

What stands out

- DraftKings reported year-over-year growth in Q1 2026, with revenue and customer trends moving in the right direction.

- The update signals continued demand for online sports betting and iGaming in regulated US markets.

- Customer acquisition still matters, but retention and product depth look just as central now.

- Investors should watch margin discipline as closely as revenue growth.

DraftKings Q1 2026 growth in plain English

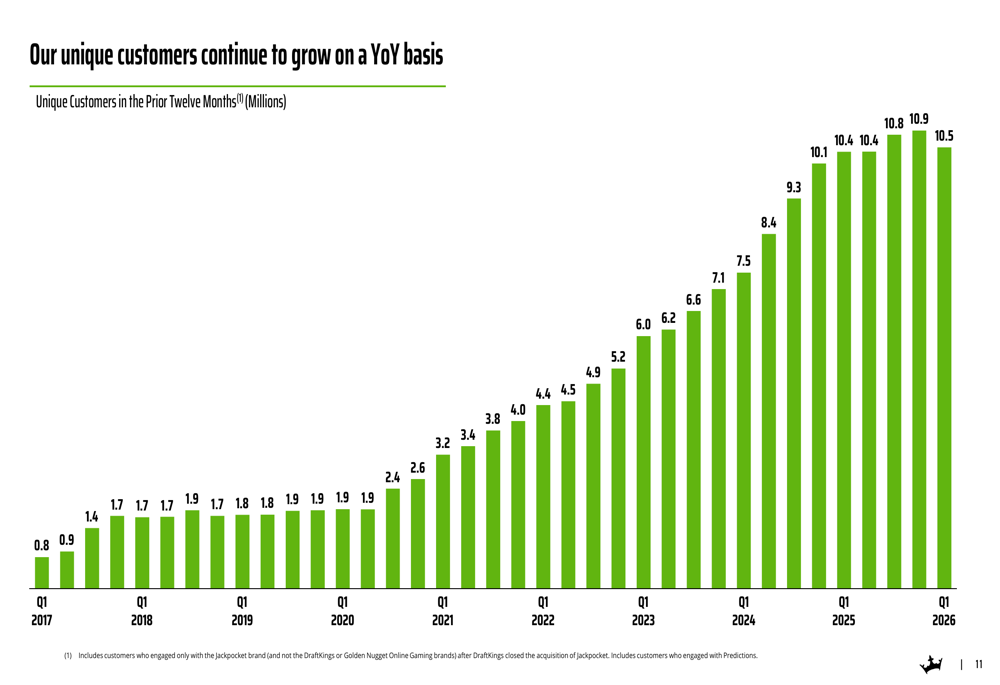

DraftKings said its first-quarter 2026 results showed growth across core parts of the business, continuing a pattern that market watchers have come to expect from the company. That includes higher revenue and stronger engagement from customers using its sportsbook and online casino products.

Here is the simple version. More people are betting, existing users are staying active, and DraftKings is getting more value from the markets where it already operates. That is often a healthier signal than pure expansion alone.

Growth is easy to celebrate. Efficient growth is what separates a solid operator from an expensive one.

And that is the real test here.

Why DraftKings Q1 2026 growth matters beyond one quarter

Quarterly growth stories are common in betting. Sustained growth in a maturing market is harder. The US online gambling sector is no longer in its land-grab phase in quite the same way it was a few years ago, so each strong report now says more about execution than simple market novelty.

Look, that changes the frame. DraftKings is no longer judged only on how fast it can add users. It is judged on whether it can keep them, cross-sell products, manage promotional costs, and improve profitability while competition stays fierce.

Think of it like a football club that has already signed its star players. At that point, fans stop caring about transfer headlines and start watching whether the team can actually win ugly on a cold away night. Same idea.

What likely drove the quarter

1. Stronger customer activity

Growth quarters in this sector usually rest on active users and spending per user. If DraftKings posted stronger first-quarter numbers, that suggests healthy engagement across major betting events and a customer base that kept coming back.

That repeat behavior matters more than flashy signup spikes. One-off traffic is nice. Habit is where the money is.

2. Product mix across sportsbook and iGaming

DraftKings benefits from operating in both online sports betting and iGaming where regulation allows it. That mix can soften the seasonal swings that pure sportsbook operators face. Sports betting drives acquisition. Online casino often drives steadier revenue over time.

Honestly, this is one of the cleaner strategic advantages in the market. A customer who uses both products is usually worth more and tends to stick around longer.

3. State-by-state market maturity

Some regulated states are now old enough to produce more predictable customer behavior. That helps operators tune marketing spend, promos, and retention offers with more precision. In plain terms, they waste less money chasing low-value traffic.

And yes, that matters a lot if you care about earnings quality.

Questions investors and operators should ask

- How much of the growth came from real engagement versus heavy promotions? Revenue growth looks better when it is not bought at an unsustainable cost.

- Did average revenue per user improve? That can say more about product strength than headline customer counts.

- How did DraftKings manage costs? A betting operator can post a loud quarter and still leave a mess underneath.

- What came from new markets versus existing ones? Growth from mature states often carries more weight.

These are not small details. They are the difference between a sharp quarter and a pretty press release.

What this means for the wider US betting market

DraftKings remains one of the clearest bellwethers for regulated online gambling in the United States. When it grows, it can reflect broad consumer demand, stronger digital betting habits, and the staying power of mobile wagering.

But rivals should not read this as proof that scale alone solves everything. FanDuel, BetMGM, Caesars, and other operators are all trying to squeeze more value from the same customers. The fight now is less about showing up and more about product speed, pricing, same-game parlays, casino content, and user experience.

That is where a lot of these battles will be won. Quietly, too.

What the earnings signal says about DraftKings strategy

The company appears to be following a familiar but sensible path. Build market share, deepen customer engagement, improve efficiency, and lean harder on owned tech and data. For a public company in this space, that is the non-negotiable sequence.

A few strategic themes stand out:

- Retention over pure acquisition. Keeping profitable players active is cheaper than replacing them.

- Cross-sell strength. Sportsbook users who move into iGaming can lift lifetime value.

- Operational discipline. Better quarters invite scrutiny on margins, not applause alone.

- Brand staying power. In a crowded market, familiar names still carry weight.

There is also a perception angle. Strong results help DraftKings look less like a growth story running on adrenaline and more like a real operating business with a durable base.

What could slow the story down

No earnings report exists in a vacuum. DraftKings still faces the same pressures that stalk every major US operator. Regulatory friction, tax changes, promo wars, and slower state expansion can all hit momentum.

What happens if customer acquisition costs rise again? That is the kind of question worth asking before anyone gets carried away.

Another issue is market saturation in established states. Once the easy users are gone, operators need better product design and sharper retention systems to keep growth moving. That takes skill, not noise.

How to read the next quarter

If you want a better handle on where DraftKings is headed, watch a short list of signals instead of just the headline revenue figure.

- Monthly unique payers or equivalent customer activity metrics

- Average revenue per user trends

- Marketing and promotional efficiency

- Adjusted earnings direction

- Performance in mature states compared with newer launches

That mix tells you whether the business is building on bedrock or on soft sand (and public markets usually figure out the difference fast).

Where this goes next

DraftKings Q1 2026 growth looks like a good sign for the company and a useful signal for the sector. It points to demand that is still healthy and a business that may be getting sharper as the market ages. Still, strong quarters earn attention. They do not earn blind trust.

The next step is simple. Watch whether DraftKings can turn this growth into cleaner margins, steadier customer value, and fewer questions about the cost of staying ahead. If it can, the company strengthens its case as one of the market’s defining operators. If not, the numbers will start to feel thinner than the headlines.