US Sports Betting Trends in Q1: Stable Growth, Murky Outlook

If you track operator revenue, state tax intake, or where the next legal market might open, US sports betting trends in the first quarter send a mixed signal. The top-line numbers still look healthy. Handle has held up, online betting remains the main engine, and large operators keep pulling market share. But that steady surface hides tougher questions. Growth is slowing in mature states. Promotional spending is less aggressive than it was during the land-grab years. And lawmakers are taking a harder look at tax rates, licensing terms, and the social cost of expansion. If you work in betting, payments, affiliate media, or compliance, that matters now because the easy phase is over. The next phase will depend less on launch buzz and more on margins, regulation, and whether new states actually move.

What stands out right now

- Q1 performance was steady, not explosive. That points to a market settling into a more mature pattern.

- Large operators remain in control. Scale still matters in user acquisition, pricing, product depth, and retention.

- Long-term growth looks less certain. Tax pressure and slower legalization could limit upside.

- Investors should watch hold and margin, not just handle. Big betting volume means less if costs keep climbing.

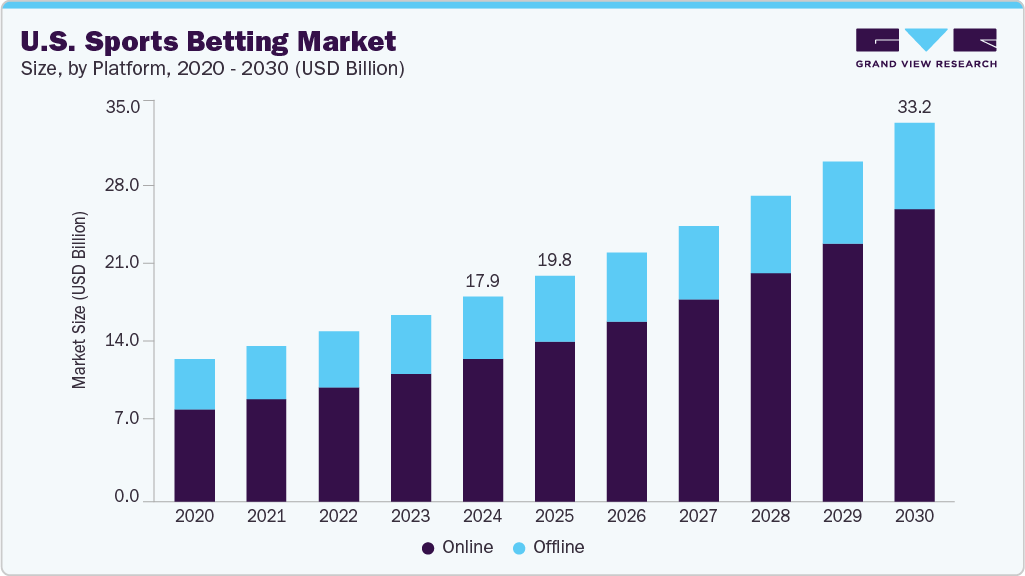

Why US sports betting trends look stable in Q1

The simple version is that online sports betting in the US is no longer a novelty. In many states, it is a routine consumer product. That changes how quarterly numbers behave. You get fewer spikes tied to launch marketing and more results driven by sports calendars, retention, and product quality.

Q1 also benefits from a packed schedule. The NFL playoffs, Super Bowl, college basketball, and the start of other major sports create reliable betting demand. That does not mean every operator wins equally. It means the category itself has a strong seasonal floor.

Steady handle can look comforting. But if hold dips or taxes rise, that same quarter can feel a lot thinner on the earnings call.

Here’s the thing. Handle alone has always been an imperfect scoreboard. It is useful, but it can flatter weak economics. A bettor can cycle a lot of money through a sportsbook while the operator ends up with a modest win rate after promos, taxes, and operating costs.

US sports betting trends by market maturity

One of the clearest ways to read US sports betting trends is to split states into three buckets. Newer markets. Expansion-stage markets. Mature markets.

Newer markets still get a pop

Fresh launches often show strong early adoption because curiosity, marketing, and pent-up demand all hit at once. But that bump fades. Fast. Once the sign-up offers cool off, the real question becomes whether the local player base keeps betting without heavy subsidy.

Expansion-stage markets fight for share

These are states where legal betting is established, but operators still think they can take share through product tweaks, parlay menus, live betting, and cross-sell from casino or DFS databases. This stage can look healthy from the outside, though margins are often under pressure.

Mature markets tell the harder truth

In mature states, growth usually slows because the market is already penetrated. That is normal. It is also where business models get tested. Can operators grow revenue without paying too much for each active user? Can they hold customers when promos shrink? Those are non-negotiable questions now.

One sentence matters more than the rest.

The market is starting to behave less like a startup sprint and more like a utility business with sports seasonality layered on top. Think of it like a football team that has moved past flashy trick plays and now has to win in the trenches. Glamour gets attention. Blocking wins games.

What could cloud the long-term outlook

The article source points to uncertainty ahead, and that caution is justified. Several forces could cap the next leg of growth.

- Tax rates are rising in some jurisdictions. Higher taxes can squeeze operator margins, reduce promo intensity, and make second-tier market entry less appealing.

- Legalization momentum is uneven. Big untapped states still face political friction, tribal issues, or moral opposition.

- Customer acquisition is getting pricier. The cheap users are gone in many markets. Retention matters more now.

- Regulatory scrutiny is sharper. Expect more debate over affordability checks, ad limits, and responsible gambling controls.

Honestly, the tax issue may be the biggest swing factor. If lawmakers keep seeing sportsbooks as an easy revenue source, operators will have to adjust. That could mean lower promotional spend, tighter risk controls, or less appetite for marginal markets.

What operators and affiliates should watch next

If you run an operator, affiliate business, or support service, it helps to shift your dashboard. Stop staring only at raw handle growth. Start tracking the quality of that growth.

- Hold percentage: Is revenue keeping pace with betting volume?

- Promo efficiency: Are bonuses creating durable users or just temporary spikes?

- State-by-state tax drag: Which markets still justify aggressive spend?

- Product mix: Are parlays, in-play betting, and same-game products lifting margins?

- Regulatory friction: Are ad rules or compliance costs changing the economics?

And affiliates should be realistic. The era of easy sportsbook CPA deals across every state is fading. More operators want better-qualified traffic, stronger retention, and compliance-safe acquisition channels. That shifts value toward trusted editorial brands and away from thin comparison pages.

What the Q1 numbers do not tell you

Quarterly reports rarely capture consumer fatigue, policy backlash, or the cost of saturation in a clean way. You have to read between the lines. A flat or slightly rising handle number can hide softer engagement, fewer new depositors, or a market leaning harder on a small group of active bettors.

But there is another angle. A slower, more disciplined market is not automatically bad. It can produce healthier businesses if operators stop chasing vanity metrics and build for retention, compliance, and sane customer economics. That is a better foundation than splashy promo wars that burn cash.

Where this leaves the industry

The first quarter suggests that sports betting in the US still has a solid base. But the next chapter will be tougher, and probably smarter. Operators with scale, efficient product teams, and strong compliance muscle should keep the upper hand. Smaller brands will need a sharper niche or a better partnership model to stay relevant.

Look, steady is fine for a quarter. It is not enough for a five-year story. The real test is whether the industry can grow without depending on endless state launches and promo-fueled sugar highs. If that answer is no, the next big betting trend will not be expansion. It will be consolidation.