Kambi Q1 Earnings Push Stock to 52-Week High

If you follow betting technology stocks, you know how rare it is for the market to reward caution. Yet that is exactly what happened after Kambi Q1 earnings landed. The sportsbook supplier did not post flashy top-line growth, but it showed something investors value just as much right now, which is tighter cost control and stronger profit margins. That matters because the sports betting supply market has become harder, pricier, and less forgiving. Operators want efficiency. Public investors want proof that a B2B betting tech company can grow without burning through margin. Kambi’s latest quarter gave them a cleaner story. And the market reacted fast, sending the stock to a 52-week high. So what actually changed, and does this move hold up once you look past the headline pop?

What stood out this quarter

- Kambi’s stock hit a 52-week high after its first-quarter report.

- Profit margins improved even though revenue growth was modest.

- Lower operating costs helped offset pressure in the sportsbook supplier market.

- Investors appear to be rewarding discipline over hype.

Why Kambi Q1 earnings moved the stock

The basic answer is simple. Margins got better.

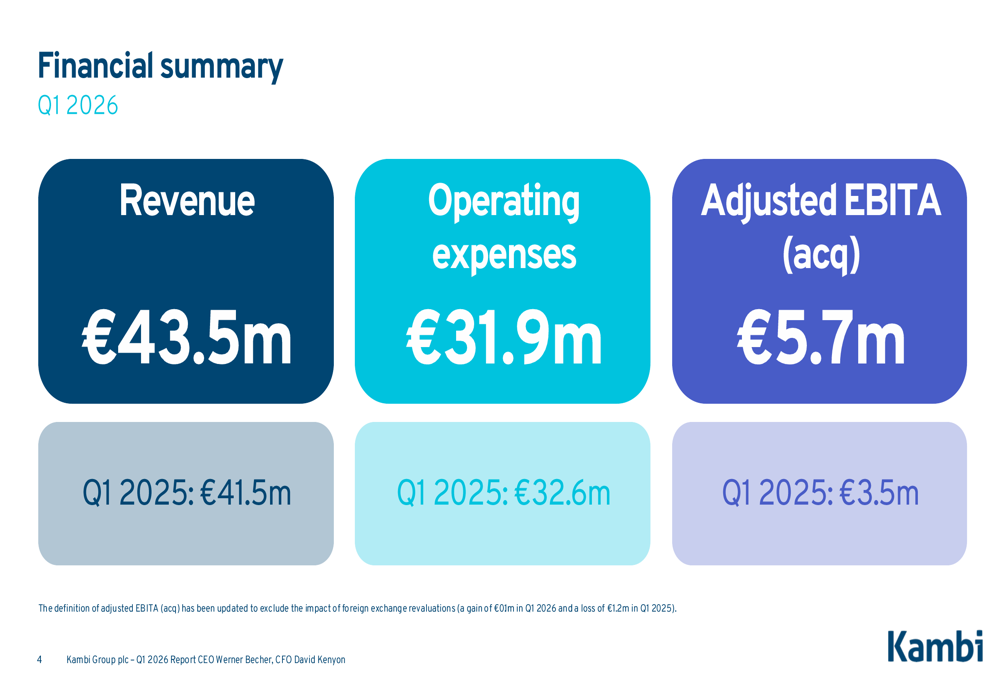

According to Legal Sports Report, Kambi reported improved profitability in the first quarter, helped by cost reductions and a more efficient operating base. For a company in betting technology, that can be more persuasive than a noisy revenue spike, especially in a market where contract wins, customer concentration, and regional regulation can all swing sentiment in a hurry.

Look, investors have heard the growth story from sportsbook suppliers for years. What they want now is evidence that the business can hold up when operators squeeze vendors on price and when major clients reassess their platform strategy. Kambi gave them a sturdier signal this quarter.

Investors did not need a perfect quarter from Kambi. They needed proof that margin repair was real.

Kambi Q1 earnings and margin improvement

The heart of the report was margin expansion. That likely explains more of the stock jump than any single revenue figure. In plain terms, Kambi showed it could keep more of each euro it brings in, and that changes the investment case.

Why does that matter so much? Because sportsbook platform providers live in a tough middle ground. They are expected to deliver product depth, pricing tech, trading expertise, compliance support, and uptime across multiple regulated markets. But they also face pressure from big operators that want lower fees or eventually want to bring parts of the stack in-house.

Kambi has dealt with that pressure for years. So a quarter that shows better operating discipline lands like a clean strike in the late innings. Not flashy, just decisive.

What likely helped margins

- Lower costs, which improved operating leverage.

- A leaner structure, suggesting management has been more selective about spending.

- Better efficiency across the business, even without explosive revenue growth.

That mix matters more than many casual readers assume. A supplier can survive a slow patch in revenue if its cost base is under control. The reverse is much uglier.

What this says about the betting tech market

This quarter says as much about the market as it does about Kambi itself. The old public-market script for gambling tech was straightforward. Win licenses, add partners, enter new states or countries, and let growth carry the story. That script has aged.

Now the questions are tougher. Can you defend pricing? Can you keep clients? Can you build product without overspending? And can you do all that while regulators keep changing the rules?

Kambi’s report suggests investors are adjusting to this new reality. They are placing more weight on execution and less on broad promises. Honestly, that is overdue.

There is also a wider lesson here for B2B gambling companies. If you are not one of the giant operators, your path to market credibility has to run through discipline. The days when the sector could skate by on expansion headlines alone are fading.

Should investors read this as a turning point?

Maybe, but not without caveats.

A strong margin quarter is meaningful, though one quarter does not erase the structural questions around Kambi’s long-term position in sportsbook technology. The company still operates in a sector where client churn, in-house platform moves, and competition from other suppliers can reshape the picture quickly.

That is the tension. The quarter was clearly positive. But the bigger debate remains open.

If you are evaluating this as a turning point, focus on a few practical markers:

- Whether margin gains continue over the next several quarters

- Whether revenue stabilizes or improves alongside cost discipline

- Whether Kambi can deepen relationships with existing partners

- Whether product investment remains sharp without inflating expenses

That last point matters a lot. Cutting costs is useful. Cutting into your own product edge is something else entirely.

How Kambi’s position compares with operator-owned tech

One reason Kambi is watched so closely is that it sits at the center of a wider fight in sports betting. Should operators outsource core sportsbook tech, or should they own more of it themselves?

Kambi’s model still makes sense for operators that want speed, market access, and proven trading infrastructure without building every piece from scratch. That approach can save time and lower execution risk, particularly in regulated markets where compliance mistakes are expensive.

But larger operators often want more control over margins and product direction. That is why supplier relationships can be both valuable and fragile.

Think of it like renting a commercial kitchen versus building your own restaurant facility. Renting gets you operating faster and with fewer headaches. Owning gives you more control later, if you can afford the cost and complexity. Kambi’s job is to keep making the rental option look smart.

What smart readers should watch next

If you cover or invest in gambling stocks, the next few quarters will matter more than the headline spike. Here is where I would keep my eyes.

1. Margin durability

Was this a one-off improvement, or the start of a steadier pattern? Sustainable margin gains would carry real weight.

2. Client momentum

New deals and partner retention still shape Kambi’s long-term ceiling. Better margins are helpful, but supplier businesses need dependable customer flow.

3. Product competitiveness

Can Kambi keep its sportsbook platform attractive while staying lean? That balance is non-negotiable.

4. Market sentiment toward gambling tech

Sometimes a stock move reflects company progress. Sometimes it reflects a broader shift in how investors price the whole sector. Usually, it is some of both.

Where this leaves Kambi

Kambi did what it needed to do this quarter. It gave investors a more convincing efficiency story, backed by better margins and tighter cost control, and that was enough to push the stock to a 52-week high.

But the real test is still ahead. Can Kambi Q1 earnings mark the start of a longer run of disciplined execution, or will this look like a brief rally in a hard market? That is the question worth tracking, and the next report should give a much sharper answer.