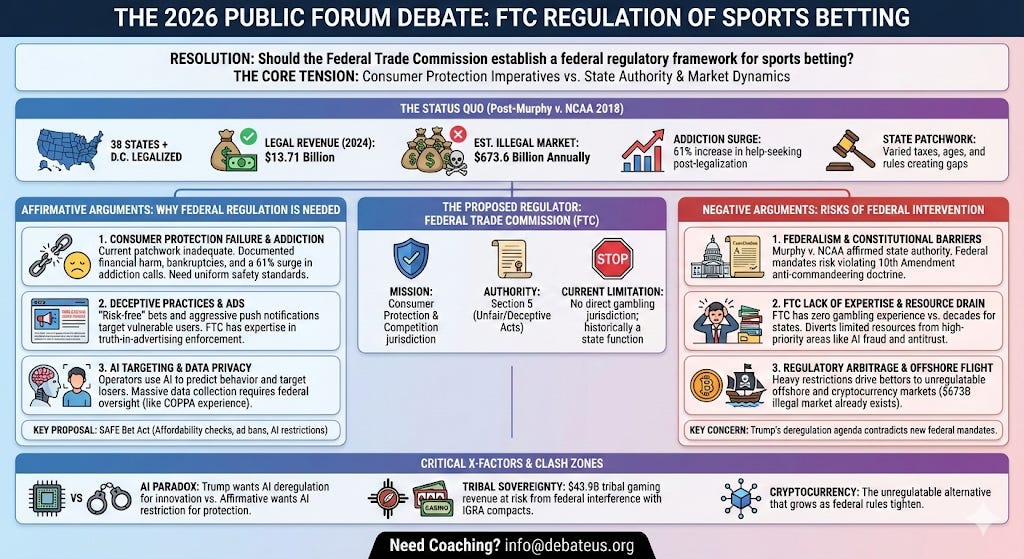

Gensler Challenges Fed on Sports Betting Oversight

The fight over sports betting oversight is getting sharper, and that matters if you run a book, build for one, or watch regulation for a living. Gary Gensler’s criticism of the Federal Reserve’s role in parts of the payment and compliance stack puts fresh attention on a system that already feels stitched together from different rulebooks. That kind of overlap creates friction fast. Who is responsible when a wager, a payment, or a consumer protection issue crosses agency lines?

That question is not academic. It affects how operators move money, how regulators share authority, and how much risk payment firms are willing to carry. And when the rules are murky, the people with the least room to absorb mistakes are usually the ones doing the day-to-day work. Look closely and you can see the problem. Sports betting has grown faster than the oversight model built around it.

Why the sports betting oversight dispute matters

- Regulatory overlap creates delays for operators trying to stay compliant.

- Payment controls sit at the center of most sports betting oversight debates.

- Clearer authority could reduce friction for banks, fintechs, and sportsbooks.

- Compliance teams need cleaner rules before they can scale safely.

Gensler’s issue is not really about one speech or one agency. It is about the patchwork nature of U.S. gambling regulation. State gaming boards, federal financial regulators, payment processors, and anti-money-laundering rules all touch the same transaction. That is a lot of hands on one wheel.

Regulation works best when the lines are boring. The moment every transaction needs a legal map, costs rise and mistakes multiply.

What Gensler is pushing back on

The core complaint is about responsibility. If a payment flow connected to sports betting raises compliance concerns, which agency takes the lead? The Fed focuses on monetary stability and banking supervision. The SEC chief, by contrast, is used to market oversight and enforcement. Those are different jobs, and the overlap can get messy.

For sportsbooks and their vendors, the result is a familiar headache. One regulator may care most about consumer protection, another about bank risk, and another about state licensing. That leaves operators trying to satisfy multiple masters at once (which is expensive, slow, and often a little absurd).

Why payments sit at the center

Sports betting is a payments business as much as it is an entertainment business. Deposits, withdrawals, fraud checks, chargebacks, and identity verification all run through financial rails. If those rails tighten, customer experience suffers. If they loosen too much, the door opens to abuse.

That is why this dispute matters beyond Washington. A bookmaker can have strong odds pricing and a slick app, but if banking partners get nervous, growth stalls. It is like building a stadium with no parking plan. The event may be ready, but the flow is a mess.

What operators should watch next

- Bank partner behavior. Watch for stricter onboarding, more document requests, and narrower risk policies.

- Payment processor standards. Expect more scrutiny around merchant codes, transaction monitoring, and suspicious activity flags.

- State-federal coordination. Any better alignment between agencies could change compliance timelines quickly.

- Enforcement tone. If regulators start sounding less tolerant of ambiguity, vendors will feel it first.

Honestly, the biggest risk is not a headline enforcement action. It is slow drift. Banks get cautious. Processors add friction. Operators respond with heavier compliance layers. Costs creep up. That is how regulation changes the market without a single dramatic ruling.

Sports betting oversight and the next policy fight

The broader policy fight is about whether U.S. gambling regulation can keep pace with a digital product that moves money in seconds. Sportsbooks now sit inside a financial system that was not designed around in-game wagering, promo abuse, or rapid-fire deposits. The current setup works, but only barely.

Could a cleaner division of duties fix that? Maybe. But better coordination between the Fed, the SEC, and gaming regulators would likely help more than another layer of rules. The industry does not need louder oversight. It needs clearer lines.

For now, operators should treat this as a signal, not a side story. Build compliance programs that assume closer scrutiny. Tighten payment reviews. Stress-test vendor contracts. The next round of sports betting oversight may not come from one agency alone, and that is exactly why the sector should prepare now.

What happens if the lines stay fuzzy?

If the agencies keep talking past each other, the market will keep paying for the confusion. Smaller operators will feel it first. Larger ones will adapt, but only by spending more on legal, compliance, and payments infrastructure.

That is the real story here. Sports betting is no longer a niche policy issue. It is a test of whether U.S. regulators can manage a fast-moving consumer market without tripping over each other. The next move from Washington will tell you a lot.