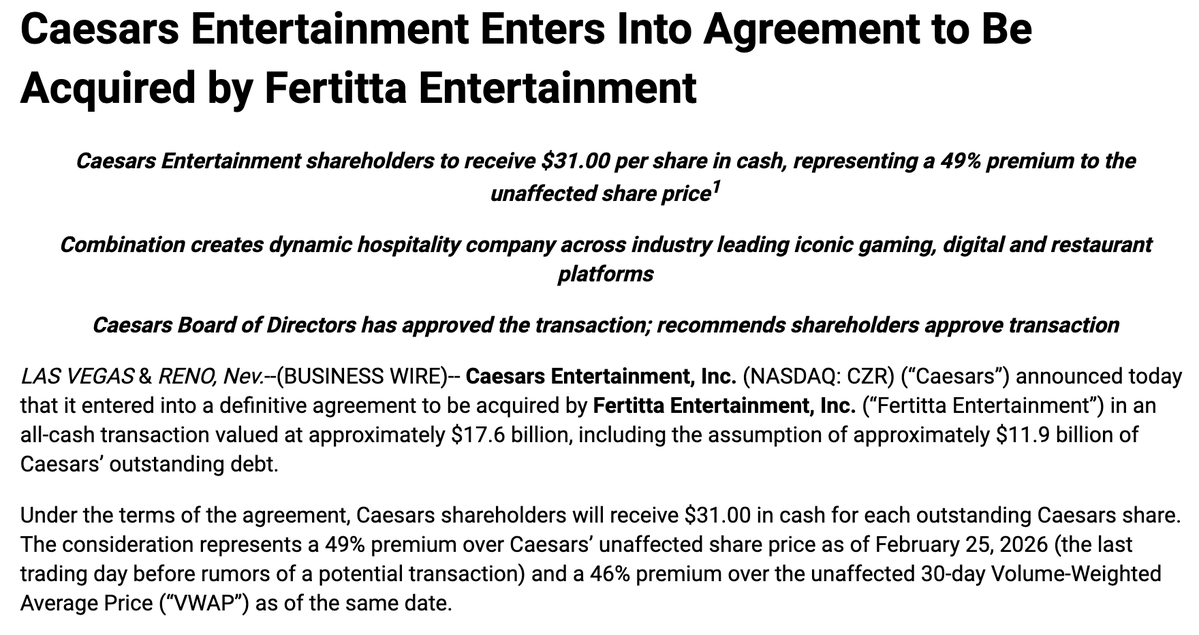

Fertitta Entertainment Caesars acquisition: what the $17.6B deal means

If you track casino M&A, the reported Fertitta Entertainment Caesars acquisition is the kind of deal that forces a reset. A $17.6 billion transaction would reshape the U.S. gaming map, put another major Las Vegas name under the Fertitta umbrella, and raise hard questions about regulation, debt, and operating strategy. That matters now because scale is no longer a nice extra in gaming. It affects market access, loyalty programs, online betting ties, and financing power.

Investors, operators, and suppliers all need the same thing. A sober read on what this move could actually change. The headline number is big, but the real story sits underneath it. Who gains pricing power? Where do regulators push back? And can a combined business run lean enough to justify the cost?

What stands out

- The reported price tag is massive. At $17.6 billion, this would rank among the most watched gaming deals in recent memory.

- Scale is the point. A larger footprint can strengthen loyalty ecosystems, regional cross-sell, and negotiating power with partners.

- Regulators will matter as much as financiers. State gaming boards and antitrust review could shape the final structure.

- Execution risk is real. Casino mergers look clean on paper, but systems, staffing, and brand strategy can get messy fast.

Why the Fertitta Entertainment Caesars acquisition matters

Caesars is not a niche asset. It is one of the most recognized names in U.S. gaming, with reach across regional casinos, Las Vegas, and digital betting relationships. If Fertitta Entertainment takes control, it gets more than properties. It gets customer data, loyalty depth, and a louder voice in the market.

Look, this is where hype often outruns reality. Bigger does not always mean better. But in gaming, scale can work like a well-built airport hub. More routes feed more passengers, and more passengers make every route more valuable. The same logic applies to casino databases, player rewards, hotel inventory, food and beverage, and event programming.

In casino dealmaking, the purchase price grabs attention. The operating model decides whether the deal was smart.

What Fertitta may be buying beyond the headline

The obvious assets are casinos, hotels, and real estate-linked cash flow. The less obvious value sits in the customer machine around those assets. Caesars has long leaned on brand reach and rewards infrastructure to move players across markets. That engine can be worth more than any single property.

1. Loyalty and database strength

Player databases are a non-negotiable asset in modern gaming. They help operators target offers, fill rooms midweek, and shift customers between regional venues and destination resorts. A bigger database also supports digital partnerships, where operators need low-cost customer acquisition instead of endless promo burn.

2. Regional diversification

Regional gaming can smooth volatility better than relying too heavily on one destination market. If one market softens, another can keep cash flow steady. That kind of spread matters when financing costs stay high.

3. Operating leverage

Every buyer talks about synergies. Some are real. Shared procurement, unified tech systems, tighter marketing spend, and overlapping corporate functions can trim costs. But there is always a catch. You only get those savings if integration is disciplined, and that takes time.

That is the hard part.

Fertitta Entertainment Caesars acquisition and the regulatory test

Any serious read on the Fertitta Entertainment Caesars acquisition has to start with regulators. Gaming is not like buying a generic consumer brand. State regulators examine ownership suitability, financial structure, licensing exposure, and competitive concentration. And antitrust eyes may focus on local or regional overlap, not just the national picture.

Could the deal face pushback? Of course. In some jurisdictions, authorities may want divestitures or operating safeguards if market share gets too concentrated. The exact pressure points would depend on property overlap, supplier relationships, and how the buyer plans to structure control.

Honestly, this is where many merger stories go off the rails. Commentators treat approval as a formality. It is not. Gaming regulators tend to look past flashy investor presentations and ask a blunt question: does this structure protect market integrity and the public interest?

What investors should watch next

If you are assessing the reported deal, focus less on headlines and more on a handful of signals. They will tell you whether this is a disciplined expansion or an expensive bet dressed up as strategy.

- Financing mix. Watch how much debt, equity, and asset-level structuring supports the transaction. The capital stack will shape future flexibility.

- Management control. Who actually runs integration, and how much autonomy stays with existing Caesars leadership?

- Property overlap. Overlap creates both synergy potential and antitrust risk.

- Digital strategy. Caesars has sports betting and iGaming relevance through market access and customer ties. Any buyer needs a clear digital plan.

- Real estate posture. Will core assets stay in place, or does the deal open the door to sales, leases, or portfolio reshuffling?

What this could mean for the wider casino sector

A deal this large would send a message across the market. If it lands, rivals will revisit their own scale gaps, regional exposure, and capital plans. Smaller operators may suddenly look more attractive as bolt-on targets. Suppliers could also face a tougher negotiating environment if another buyer grows purchasing power.

And workers, partners, and host cities will be watching for a different reason. Large gaming mergers often promise efficiency. That can mean investment in top assets, but it can also mean cuts in duplicate roles or slower spending elsewhere. The balance matters.

The part the headline misses

The source report centers on the deal value, which is fair. But the sharper question is whether Caesars is being valued as a set of properties or as a platform. Those are two very different things. A property buyer looks for cost cuts and asset cash flow. A platform buyer wants cross-market customer movement, digital upside, and long-term control over demand.

That distinction matters because the integration plan will follow it. Think of it like coaching a deep baseball roster. If you only count home runs, you miss defense, depth, and bullpen management. Casino groups work the same way. The visible assets matter, but the hidden system often decides who wins.

Where this story could go from here

For now, caution makes sense. Deal reports can move faster than confirmations, and final terms often shift once financing and regulatory review get serious. Still, the strategic logic is easy to see. Fertitta has a history of building consumer-facing businesses, and Caesars offers a broad stage if the numbers and approvals line up.

If this transaction progresses, watch for details, not slogans. The purchase price matters. The structure matters more. And if the Fertitta Entertainment Caesars acquisition does become real, the next question is simple: will this create a stronger casino operator, or just a larger one?